M.Sc. Tim Janke

Probabilistic price forecasting for electricity markets

Research Interest

General research interests:

- Machine learning and data analysis in the energy domain

- Uncertainty quantification

- Probabilistic forecasting

- Energy market design & regulation

Current project: probabilistic price forecasting for electricity markets

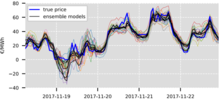

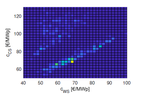

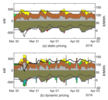

In the course of the Energiewende the share of renewable energy sources (RES) in the total electricity generation has steadily increased. One main characteristic of RES is their dependence on the given supply, i.e. solar radiation or wind speed, which renders the expected production from these sources volatile and uncertain. This motivates the efforts currently undertaken to increase the ability of the demand side to react flexible to the increasingly volatile generation. Furthermore, the markets for energy and power gained in importance. Market prices play the key role for the effective and efficient coordination of the volatile and uncertain generation from RES, the thermal generation, and the flexible share of the demand. Operators of flexibility options, such as storages, industrial processes, gas turbines, or heat pumps, must decide at all times on bid prices and quantities as well as on the market at which they place their offer under an uncertain future market price. Hence, the operators face a complex stochastic optimization problem with the market price as the key parameter.

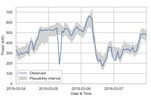

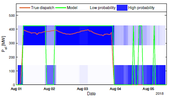

Therefore, the goal of the project is to develop and validate methods and algorithms for the reliable probabilistic forecasting of electricity prices for several markets. A probabilistic forecast, i.e. a forecast of a probability distribution for each point in time instead of just a single, most likely value, enables the application of stochastic optimization methods because it allows the incorporation the of uncertainty of the prediction. This is especially relevant in times of high volatility or extreme prices events. The developed methods should help to encourage and facilitate the active participation of small and medium sized suppliers, prosumers, and consumers in modern energy markets.

The project is done in cooperation with the Entega AG and funded by the TU Darmstadt Pioneer Fund.

![]()

Open theses

Unfortunately, there is nothing available in the moment.

Short Bio

Since 2017: PhD student at EINS

2013 – 2017: M.Sc. Business Administration/Industrial Engineering at TU Darmstadt and University of Bergamo

2008 – 2013: B.Sc. Business Administration/Industrial Engineering at TU Darmstadt

Publications

[Journal]

Mario Beykirch; Andreas Bott; Tim Janke; Florian Steinke :

The Value of Probabilistic Forecasts for Electricity Market Bidding and Scheduling Under Uncertainty.

In: IEEE Transactions on Power Systems , 2024

[Journal]

Jieyu Chen; Tim Janke; Florian Steinke; Sebastian Lerch :

Generative machine learning methods for multivariate ensemble post-processing.

In: Institute of Mathematical Statistics Annals of Applied Statistics , 2023

[Journal]

Andreas Bott; Tim Janke; Florian Steinke :

Deep learning-enabled MCMC for probabilistic state estimation in district heating grids.

In: Elsevier Applied Energy 336 , P. 120837, prePrint, 2023

[Conference]

Mario Beykirch; Tim Janke; Florian Steinke :

Bidding and Scheduling in Energy Markets: Which Probabilistic Forecast Do We Need?.

In: 17th International Conference on Probabilistic Methods Applied to Power Systems (PMAPS 2022), virtual Conference, 2022

[Conference]

Mario Beykirch; Tim Janke; Imed Tayeche; Florian Steinke :

Probabilistic Forecast Combination for Anomaly Detection in Building Heat Load Time Series.

In: 2021 IEEE PES Innovative Smart Grid Technologies Conference Europe (ISGT-Europe), virtual Conference, 2021

[Conference]

Tim Janke; Mohamed Ghanmi; Florian Steinke :

Implicit Generative Copulas.

In: 35th International Conference on Neural Information Processing Systems (NeurIPS 2021), virtual Conference, 2021

[Conference]

Tim Janke; Florian Steinke :

Probabilistic multivariate electricity price forecasting using implicit generative ensemble post-processing.

In: 16th International Conference on Probabilistic Methods Applied to Power Systems (PMAPS 2020), virtual Conference, 2020

[Journal]

Tim Janke; Florian Steinke :

Forecasting the Price Distribution of Continuous Intraday Electricity Trading.

In: Energies 12 (22), P. 4262, 2019

[Conference]

Mario Beykirch; Tim Janke; Florian Steinke :

Evaluation of Day-Ahead Electricity Price Predictions with Multi-Stage Stochastic Programs.

In: 8th International Ruhr Energy Conference (INREC 2019), Essen, Germany, 2019

[Conference]

Mario Beykirch; Tim Janke; Florian Steinke :

Bayesian Inference with MILP Dispatch Models for the Probabilistic Prediction of Power Plant Dispatch.

In: 16th International Conference on the European Energy Market (EEM), Ljubljana, Slovenia, 2019

[Conference]

Mario Beykirch; Tim Janke; Florian Steinke :

Learning Dispatch Parameters of Thermal Power Plants from Observations.

In: 8th IEEE PES Innovative Smart Grid Technologies Conference Europe, Sarajevo, Bosnia-Herzegovina, 2018

[Conference]

Tim Janke; Bastian Brindley; Tobias Rodemann; Florian Steinke :

Incentivizing the adoption of local flexibility options: A quantitative case study.

In: 15th International Conference on the European Energy Market (EEM'18), Lodz, Poland, 2018